Car ownership cost breakdown: depreciation, fuel, insurance, maintenance, registration, and parking.

I’ve spent years researching and managing car expenses for myself and clients. This article explains the car ownership cost breakdown in clear, practical terms. You will learn each cost category, how to calculate yearly and monthly totals, and smart ways to cut spending. I draw on hands-on experience, industry data, and simple math to give you an actionable guide you can use today.

Understanding car ownership cost breakdown

Car ownership cost breakdown means adding every expense you pay to buy, run, and maintain a vehicle. It covers one-time costs and recurring bills. Knowing the full breakdown helps you pick the right car and budget correctly. I’ll show you step-by-step how to estimate real costs, not just sticker prices.

Fixed versus variable costs

Fixed costs stay the same each month or year. Variable costs change with use.

Fixed costs include:

- Depreciation: The car’s loss in value each year.

- Loan payments: Principal and interest on financing.

- Insurance premiums: Often billed monthly or annually.

- Registration and taxes: Annual or biennial state fees.

Variable costs include:

- Fuel or EV charging: Depends on miles driven.

- Maintenance and repairs: Oil changes, brakes, and unexpected fixes.

- Tires and consumables: Worn parts replaced by use.

- Parking, tolls, and tickets: Varies by location and habits.

Understanding which costs are fixed helps you plan a baseline budget. Tracking variable costs helps control spending by changing behavior or vehicle choice.

Major line items explained

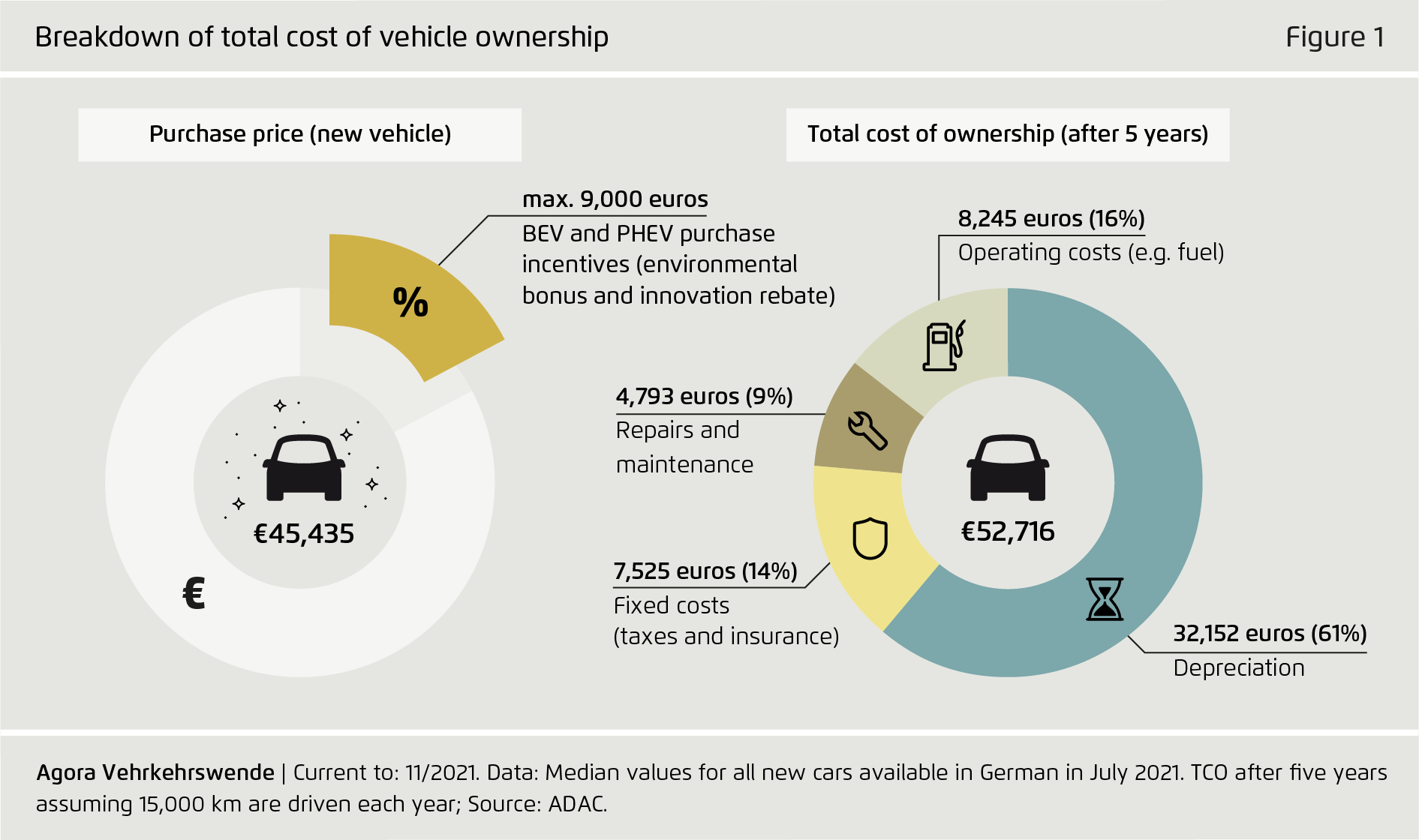

Depreciation

Depreciation is usually the largest single cost in the car ownership cost breakdown. New cars lose value fastest in the first three years. Estimate depreciation by comparing purchase price to expected resale value. For example, a $30,000 car that resells for $18,000 after five years lost $12,000, or $2,400 per year.

Financing and interest

Loan interest adds to your total ownership cost. Longer loans lower monthly payments but increase total interest paid. Compare loan terms and factor the total interest into annual cost. A lower APR and shorter loan term reduce the financing portion of the car ownership cost breakdown.

Insurance

Insurance varies by driver age, location, driving record, vehicle model, and coverage level. Full coverage costs more but protects more. Shop rates and raise deductibles where safe to lower premiums. Insurance can be a predictable part of the car ownership cost breakdown if you review it yearly.

Fuel and energy

Fuel or electricity is a variable but frequent cost. Estimate by multiplying your annual miles by your vehicle’s MPG (or kWh/mi for EVs) and local fuel price. For example, 12,000 miles/year at 30 MPG and $3.50/gallon costs about $1,400/year. Fuel habits significantly affect the car ownership cost breakdown.

Maintenance and repairs

Routine maintenance is predictable. Major repairs are not. Budget for scheduled service and set aside an emergency fund for repairs. A common rule is $500–$1,000 per year for maintenance on average vehicles, and more for older cars. Maintenance habits influence the long-term car ownership cost breakdown.

Tires, brakes, and consumables

Tires wear with miles and driving style. Brakes, wipers, bulbs, and fluids are small costs but add up. Include these in your annual estimate. Quick checks and timely replacements reduce bigger repair bills later in the car ownership cost breakdown.

Registration, taxes, and fees

Registration and state taxes are required by law. Some states tax vehicle purchases or impose higher annual fees. These costs are predictable and must be part of your total car ownership cost breakdown.

Parking and tolls

Urban drivers often pay significant parking and toll fees. Monthly parking can exceed $200 in some cities. If you commute downtown, include realistic parking and toll estimates when building your car ownership cost breakdown.

Unexpected costs and depreciation shocks

Think about loss from accidents or major mechanical failures. Extended warranties can reduce risk but cost more upfront. Unexpected events can spike the car ownership cost breakdown suddenly, so a contingency fund is wise.

How to calculate your annual and monthly cost

Follow these steps to get a realistic car ownership cost breakdown for one year.

- List fixed annual costs.

- Include depreciation, insurance, registration, and loan interest.

- Estimate variable annual costs.

- Add fuel, maintenance, tires, parking, and tolls.

- Add occasional big-ticket items.

- Plan for one-time repairs or major services.

- Sum all amounts for annual cost.

- Divide by 12 to get monthly cost.

Example calculation:

- Depreciation: $2,400/year

- Insurance: $1,200/year

- Fuel: $1,400/year

- Maintenance: $600/year

- Registration/taxes: $200/year

- Parking/tolls: $600/year

Total annual: $6,400

Monthly cost: $533

Run this math with your real numbers to get an accurate car ownership cost breakdown. Revisit figures each year as values change.

Ways to reduce your car ownership cost breakdown

Small changes make big differences. Try these practical tips.

- Buy used or certified pre-owned to reduce depreciation.

Used cars often have slower depreciation and lower purchase prices. - Choose a fuel-efficient or electric vehicle if you drive a lot.

Lower fuel costs reduce the largest variable in the car ownership cost breakdown. - Improve your credit score before financing.

Better credit means lower APR and less interest over time. - Shop insurance annually and bundle policies.

Switching carriers or increasing deductibles can lower premiums. - Perform regular preventive maintenance.

Simple checks stop small issues from becoming expensive repairs. - Reduce parking costs by carpooling or using transit occasionally.

Parking savings directly lower your monthly totals in the car ownership cost breakdown. - Consider leasing for lower monthly payments, but watch total cost.

Leasing can lower short-term costs but may increase long-term spending if used repeatedly.

These tactics can cut your annual cost significantly and improve the clarity of your personal car ownership cost breakdown.

Personal experience and lessons learned

When I bought my first new car, I focused only on the monthly payment. I later realized my real monthly cost was much higher after insurance and fuel. I switched to a used model for my next purchase and saved thousands in depreciation. I also started tracking maintenance receipts in a spreadsheet. That simple habit revealed recurring issues and helped me negotiate better with mechanics. My main lessons:

- Always calculate full annual cost, not just payments.

- Keep a repair log to spot trends.

- Factor resale value into the buying decision.

These practices made my car ownership cost breakdown predictable and easier to manage.

Tools, worksheets, and tracking tips

Use tools to keep the car ownership cost breakdown under control.

- Spreadsheets: Track expenses by category and date.

- Apps: Fuel logging, maintenance reminders, and cost trackers help automate data.

- Annual review: Recalculate your car ownership cost breakdown yearly and adjust budget.

- Maintenance schedule: Stick to manufacturer intervals to avoid costly repairs.

- Receipts and records: Keep all service and repair receipts for accuracy and resale transparency.

Tracking costs gives you power. You can spot trends and make smarter choices about repairs, upgrades, or replacing the car.

Frequently Asked Questions of car ownership cost breakdown

What typically makes up the largest portion of car ownership cost breakdown?

Depreciation is usually the largest portion, especially for new cars. It often exceeds fuel and maintenance combined in the first few years.

How much should I budget per month for car ownership cost breakdown?

A common rule is 1–2% of the car’s purchase price per month, or calculate your own by totaling annual costs and dividing by 12. Use the step-by-step calculation in this article for accuracy.

Do electric vehicles lower the car ownership cost breakdown?

They can reduce fuel and maintenance costs, but higher purchase prices and battery concerns may offset savings. Consider total cost of ownership over several years.

How can I reduce insurance costs in my car ownership cost breakdown?

Raise your deductible, maintain a clean driving record, compare quotes, and bundle policies. These moves often lower premiums without sacrificing essential coverage.

Should I buy or lease to minimize car ownership cost breakdown?

Leasing can lower monthly payments but may cost more long-term due to continuous payments and lease fees. Buying often reduces long-term cost if you keep the car several years.

How do I estimate depreciation for an older car in my car ownership cost breakdown?

Check comparable resale prices for similar cars with the same age and mileage. Subtract expected resale value from current value to estimate annual depreciation.

Can regular maintenance reduce my total car ownership cost breakdown?

Yes. Regular maintenance prevents bigger repairs and can improve fuel economy and resale value. It’s an investment that pays off over time.

What emergency fund should I keep for unexpected car ownership costs?

Aim for $1,000–$3,000 depending on the car’s age and reliability. This fund covers major repairs without derailing your budget.

Are extended warranties worth including in the car ownership cost breakdown?

Extended warranties add certainty but cost extra upfront. Compare expected repair costs and the warranty price to decide if it fits your risk tolerance.

How often should I recalculate my car ownership cost breakdown?

Annual recalculation is ideal. Revisit sooner after big changes like new loan terms, a move, or major repairs.

Conclusion

Understanding a clear car ownership cost breakdown gives you control over money and choices. Track fixed and variable costs, run the simple annual math, and use savings strategies like buying used or improving fuel efficiency. Start a cost log this week and recalculate your totals to see where you can save. Share your results, subscribe for more guides, or leave a comment about your own car ownership cost breakdown experience.