Insurance Cost Suv Vs Sedan: Which Costs More?

SUVs often cost a bit more to insure than sedans, though results vary widely by model and driver.

I have spent years working with auto insurance policies and advising drivers on value and cost. This article breaks down why insurance cost suv vs sedan often differs. I show what insurers look at, real price ranges, and hands-on tips to lower your bill. Read on for clear, practical advice based on experience and industry patterns.

Why SUVs may cost more to insure

SUVs often carry higher insurance rates for several clear reasons. They usually weigh more and can cause more damage in a crash. They cost more to repair when parts or frames are larger or specialized. Higher theft or rollover rates on some SUV models can also push premiums up. These factors mean insurance cost suv vs sedan often tips toward SUVs.

Key factors insurers consider

Insurers use simple signals to set prices. These signals explain differences in insurance cost suv vs sedan.

- Vehicle value — Higher sticker price often means higher insurance.

- Repair and parts cost — Luxury or complex parts raise claims costs.

- Safety ratings — Cars with top crash-test scores can lower premiums.

- Theft and fraud risk — Popular models for theft can be costlier to insure.

- Crash and rollover risk — Taller SUVs can have different crash profiles.

- Driver profile — Age, driving record, credit, and location matter a lot.

- Usage and mileage — More miles often equal higher insurance cost suv vs sedan.

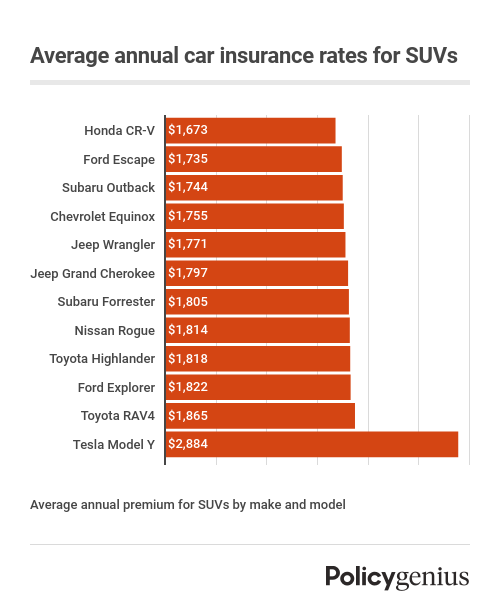

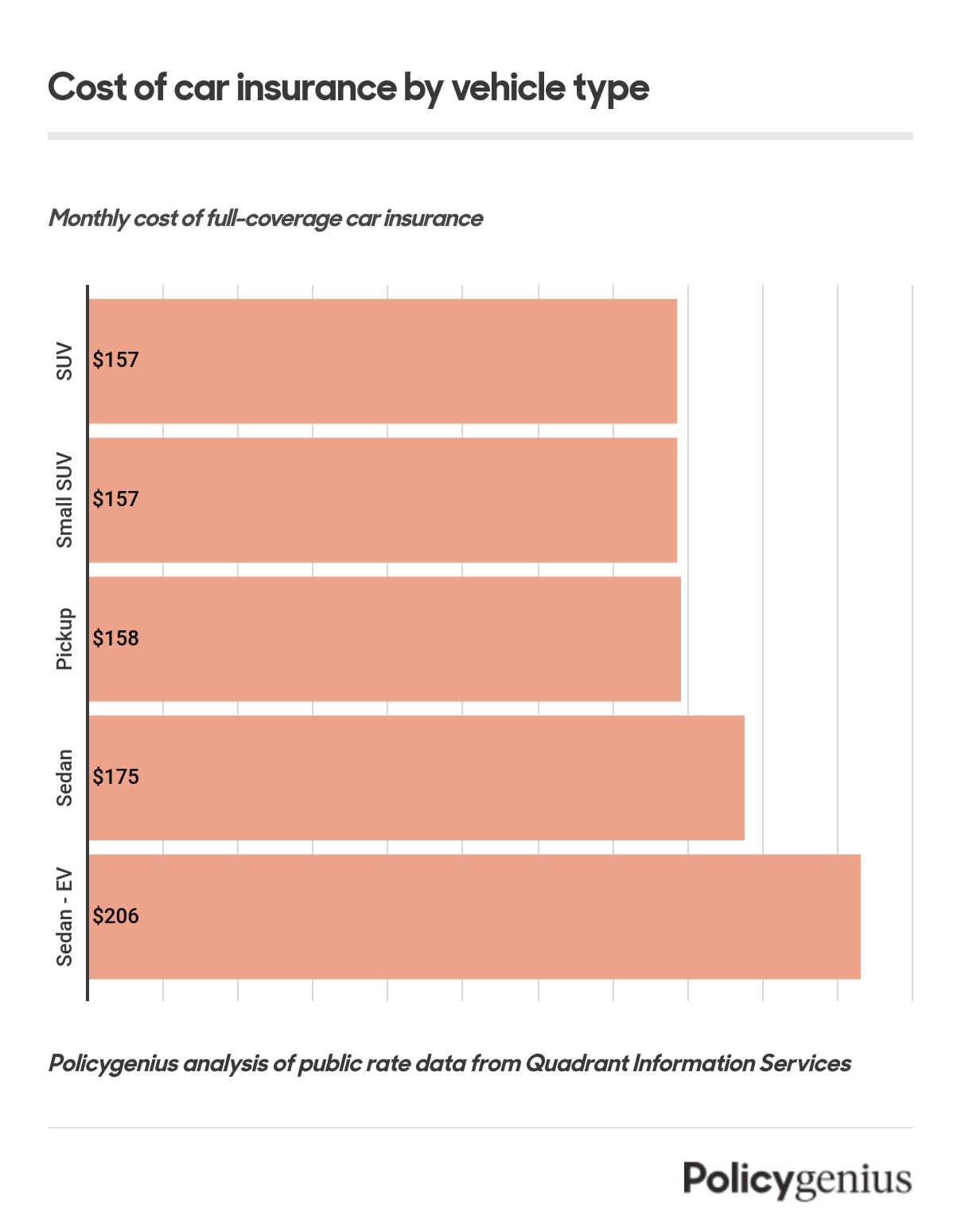

Real-world examples and typical price ranges

Expect a range, not a fixed number. For many drivers, an SUV may cost 5% to 25% more than a comparable sedan. A compact SUV might be just 5% higher than a compact sedan. A large luxury SUV can be 20% or more above a similar sedan. From my experience helping clients, switching from a mid-size sedan to a mid-size SUV raised premiums about 10% to 15% on average. Keep in mind that insurance cost suv vs sedan will shift by region, insurer, and driver history.

Practical tips to lower insurance cost for an SUV or sedan

You can cut costs with targeted moves. These tips work whether you own an SUV or a sedan and help reduce the gap in insurance cost suv vs sedan.

- Compare quotes often — Shop at least every 12 months to find better rates.

- Raise deductibles — A higher deductible lowers the premium but increases out-of-pocket risk.

- Bundle policies — Combining home and auto can bring meaningful discounts.

- Choose safety features — Anti-theft devices and advanced driver-assist features lower risk.

- Pick models wisely — Research insurance premiums before you buy.

- Keep a clean record — Safe driving history is one of the strongest discounts.

- Use usage-based programs — Low-mile or telematics plans can reduce rates.

Is buying an SUV worth the extra insurance?

The answer depends on your needs. If you need space, towing, or higher ground clearance, an SUV may be worth the extra insurance cost suv vs sedan. If you rarely use those benefits, a sedan can save money on insurance, fuel, and maintenance. I once advised a family who traded a sedan for a small SUV for safety. Their premium rose, but the comfort and cargo space matched their needs. Think about total ownership cost, not just the premium.

How to compare quotes effectively

A clear process makes comparison easy. Follow these steps to compare insurer offers and understand insurance cost suv vs sedan.

- Get the same coverage levels — Match liability, collision, and comprehensive limits.

- Ask about discounts — Look for multi-car, safe driver, and safety feature discounts.

- Check repair networks — Some insurers use specific repair shops that affect claims speed.

- Review deductible trade-offs — Compare price savings versus expected out-of-pocket.

- Read policy wording — Look for exclusions and limits that change real coverage.

- Use sample quotes for both vehicle types — Compare an SUV and a sedan with the same driver data.

Frequently Asked Questions of insurance cost suv vs sedan

How much more does an SUV cost to insure than a sedan?

On average, an SUV can cost 5% to 25% more to insure than a comparable sedan. Exact numbers depend on model, safety ratings, and driver profile.

Can safety features make an SUV cheaper to insure than a sedan?

Yes. Modern safety features and strong crash-test scores can reduce premiums and sometimes make an SUV cheaper to insure than an older sedan. Insurers reward proven safety tech.

Do repair costs drive the difference in insurance cost suv vs sedan?

Repair costs are a major driver. Larger body panels, heavy frames, and pricey parts on SUVs can raise claim costs and premiums. Cheaper, simpler models can narrow the gap.

Will my driving record affect the SUV vs sedan insurance comparison?

Absolutely. Your driving history, age, and credit score can outweigh vehicle type. A clean record may make the insurance cost suv vs sedan difference small.

Are there discounts unique to SUVs or sedans?

Discounts usually focus on features, not body style. Anti-theft devices, safety bundles, and multi-car discounts apply to both SUVs and sedans equally.

Conclusion

Choosing between an SUV and a sedan means balancing needs, comfort, and long-term cost. Insurance cost suv vs sedan often edges toward SUVs, but smart choices can shrink that gap. Compare quotes, pick safe models, and use discounts to control premiums. Take one step today: gather two quotes for the exact SUV and sedan models you like. Share your results or questions below so others can learn from your experience.